Taxing Day

- Leave a Comment

- Shortlink

- 5 min

Tax Day was over a week ago, and, as usual, I filed an extension along with hefty payment for my estimated taxes due.

However, this tax-filing season was different for two reasons. First, there was a lot of concern about the IRS’s preparedness after the most recent government shutdown, where thousands of IRS employees were furloughed for about a month. Second, this was the first filing season where most taxpayers be affected by the changes wrought by the Tax Cuts and Jobs Act of 2017. The latter is the so-called “tax-reform law” that was a gift to corporations and the rich and a temporary tax relief to some workers, while growing the federal budget deficit by trillions of dollars.

After preparing my federal return, I found that much of the hype about the complexity of the new tax laws didn’t apply to me. Instead, I was alarmed at the elimination of two key income-tax reductions that I relied on to lower my tax bill.

The Personal Exemption

Under the new tax law, the standard deduction was increased to $12,000—up from $6,350 in 2017. On its face, this is great. It allows taxpayers to shield an additional $5,650 of income from federal income tax. In other words, while in 2017, you didn’t get taxed for the first $6,350 of income you earned, in 2018, you get to take home $12,000 of income, free of federal income tax. (Note that you’re still subject to Social Security and Medicare taxes on all income you earn from work.)

However, one of the changes of the tax law was that it eliminated the personal exemption. In 2017, that amount was $4,050 for individual taxpayers with adjusted gross income less than $261,500, which I presume applies to most workers.

Without the personal exemption, the effect of raising the standard deduction didn’t actually allow workers to shield an additional $5,650 of income from taxes. It only allows them to shield an additional $1,600. That has the effect of lowering your federal income tax bill—at the 10% rate—by only $160 over an entire year. That works out to about $13 a month.

Unreimbursed Business Expenses

Most taxpayers couldn’t take this deduction, but as a part-time college teacher, I did often claim it. I work from home a lot, and I am constantly buying books, supplies, paying for subscriptions, and investing in computer hardware and software to teach and to support that work. This was especially true when teaching online classes. That work seems more suited for a 1099-type gig than a traditional W2-type job because I do a lot of that work on my own schedule—often well in advance of the actual classes—and I do not travel to campus to do that work.

Under the Tax Cuts and Jobs Act of 2017, the deduction for unreimbursed business expenses was eliminated for most workers. It only allows workers in certain fields—specifically those working in the armed forces, as qualified performing artists, as fee-based government officials—to take these deductions. These carve-outs seem curious. I can understand why we continue to allow a deduction for members of the armed forces. This is a Republican tax bill, and the GOP is party of unthinking jingoism. The same probably goes for private consultants who work for the government, replacing career government employees. But why allow performing artists to continue to take this deduction? Is it because the president was a reality TV star before entering politics and would likely return to that arena afterwards?

Without this deduction, I didn’t have enough in itemized deductions to overcome the $12,000 standard deduction. Thus, I wouldn’t receive any direct tax relief from state and local taxes—which in New York State and in New York City are substantial. Nor would I receive any direct tax relief from charitable contributions.

In effect, this tax bill eliminated incentives for me to:

1. live in a state with high taxes2

2. contribute to charity

3. invest in my job beyond the bare necessities

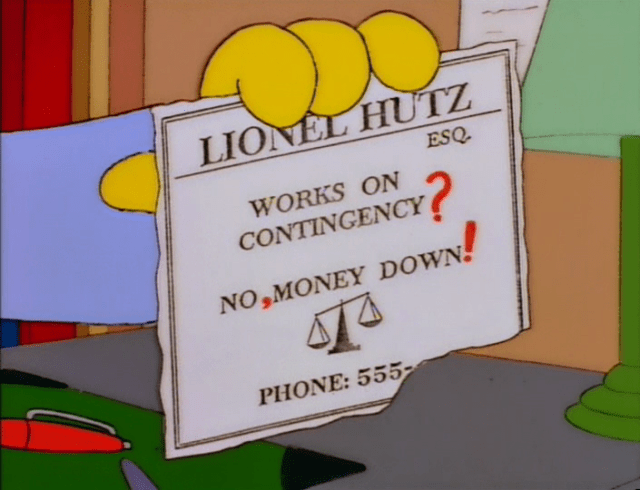

Tax [and] Cut [for] Jobs Act

In an 1990s episode of the Simpsons, “The Day the Laughter Died,” Bart consults with attorney Lionel Hutz over a legal matter. Bart expresses confusion when the attorney asks for money up-front to take their case. “But your ad says, ‘Works on Contingency. No Money Down.’” Lionel Hutz explains that the ad has some errors. He promptly corrects it read: “Works on Contingency? No, Money Down!”

This so-called Tax Cut and Jobs Act was apparently similarly misnamed. If you have a job, you saw more tax… and more cuts to your ability to reduce your tax.